Peak Earnings, Early Exit: The Silent Departure of Quantitative Finance's Most Talented Professionals

Peak Earnings, Early Exit: The Silent Departure of Quantitative Finance's Most Talented Professionals

There is a particular irony embedded in the career arc of many elite quantitative researchers. After years of doctoral-level training, grueling technical interviews, and the early grind of establishing themselves at prestigious firms, a meaningful cohort of these professionals reaches their peak earning potential — only to voluntarily surrender it. Not for a competitor. Not for a startup. For something closer to silence.

Across the United States, a quiet exodus is underway. Quantitative researchers, algorithmic traders, and financial engineers in their late twenties and early thirties are stepping away from roles that most finance professionals would consider the pinnacle of a career. The departure rate among this demographic has begun attracting attention from talent acquisition teams and senior leadership at some of the country's most competitive systematic trading operations.

The question being asked in conference rooms from Greenwich to Chicago is not simply why this is happening. It is why firms consistently fail to see it coming.

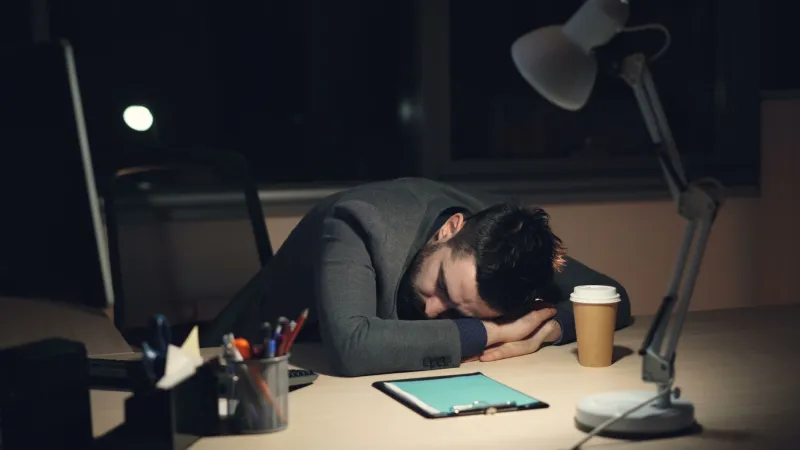

The Anatomy of Burnout in a High-Alpha Environment

Quantitative finance is not a profession that conceals its demands. The intellectual intensity is explicit from the first interview. Candidates are expected to demonstrate facility with stochastic calculus, statistical inference, and computational systems under conditions designed to simulate pressure. Those who pass are then placed into environments where the pressure never fully dissipates.

The structure of compensation in systematic trading amplifies this dynamic. Performance-linked bonuses, deferred equity, and clawback provisions create financial architectures that reward endurance as much as brilliance. The message, whether stated or implied, is that the rewards accrue to those who remain — and who continue producing at an elite level.

For many researchers, the first several years sustain themselves on the sheer novelty of the work. The problems are genuinely difficult. The intellectual stimulation is real. The compensation, particularly relative to academic alternatives, feels like validation of a choice well made.

But the environment carries costs that are rarely quantified with the same rigor applied to trading models. Sleep disruption, the erosion of personal relationships, and the psychological toll of operating in a zero-sum competitive culture accumulate in ways that do not appear on any performance review.

"There is a point at which the marginal utility of the next dollar of compensation becomes effectively zero," said one former senior researcher who departed a prominent Chicago-based proprietary trading firm at age thirty-two. "What I could not easily replace was cognitive space. The work had colonized every part of my thinking."

What the Data Suggests — and What It Obscures

Firms are understandably reluctant to publish internal attrition statistics, particularly when the departures involve high performers rather than underperformers. The talent narrative preferred by most systematic trading operations emphasizes selectivity at the point of hiring, not fragility in retention.

However, conversations with recruiters who specialize in quantitative finance placement reveal a consistent pattern. Voluntary departures among researchers aged twenty-eight to thirty-four have increased noticeably over the past several years. Notably, many of these individuals are not moving laterally to competing firms. They are taking extended sabbaticals, transitioning to academia, launching independent research projects, or exiting finance entirely.

This last category is particularly significant. The conventional assumption in quant recruiting is that elite talent cycles between firms in pursuit of better compensation or more interesting problems. The researcher who exits the industry entirely represents a different kind of loss — one that cannot be addressed by a competing offer.

The Decision Calculus Behind Early Departure

For those who have made the decision to leave, the reasoning tends to be more deliberate than the word "burnout" might suggest. These are, by professional training, individuals who approach complex problems analytically. Their departures are rarely impulsive.

Several common threads emerge from conversations with early-exit quants across New York, Chicago, and the Bay Area. The first is a recalibration of what constitutes a meaningful problem. Research environments that once felt intellectually stimulating can begin to feel narrowly constrained — particularly when the primary measure of success is P&L attribution rather than genuine scientific contribution.

The second is a growing awareness of opportunity cost in non-financial terms. Time spent optimizing execution latency is time not spent on relationships, physical health, or intellectual pursuits that carry intrinsic rather than instrumental value. As compensation scales upward, this calculus does not resolve in favor of the firm — it sharpens against it.

The third, and perhaps most structurally significant, is the absence of visible career models that suggest the trajectory improves. When the most senior researchers at a firm appear to be operating under the same constraints as junior hires — simply with larger numbers attached — the implied future becomes less compelling, not more.

What Firms Are Getting Wrong

The retention strategies most commonly deployed by quant firms in response to early-career burnout tend to be financially oriented: accelerated vesting schedules, retention bonuses, expanded profit-sharing arrangements. These instruments are not without effect. They do retain some researchers who might otherwise leave. But they address the symptom rather than the underlying condition.

More sophisticated firms have begun experimenting with structural interventions. Sabbatical programs, reduced-intensity research rotations, and explicit carve-outs for exploratory work that is not tied to near-term trading performance have appeared at several leading systematic shops. The results have been mixed, in part because cultural norms around intensity are difficult to modify without leadership-level commitment.

The firms making the most meaningful progress on retention tend to share a common characteristic: they treat intellectual autonomy as a genuine resource rather than a rhetorical one. Researchers who feel they are pursuing problems of their own choosing — even within a commercially oriented framework — report substantially different relationships with their work than those who feel instrumentalized by it.

Implications for the Broader Talent Market

The early-exit phenomenon carries implications that extend beyond individual firms. The quantitative finance industry as a whole has built its competitive advantage on a relatively small pool of exceptional talent. When a meaningful fraction of that talent voluntarily withdraws from the market before reaching its full professional maturity, the aggregate effect on research quality and innovation is not trivial.

For professionals currently navigating these questions — whether they are weighing a departure, evaluating a new role, or attempting to structure their current position more sustainably — the central insight may be this: the firms most worth working for are those that have internalized the cost of losing exceptional people. They are not common, but they exist. Identifying them requires looking beyond compensation disclosures to the less legible signals of culture, autonomy, and long-term institutional investment in the people doing the work.

The alpha, in this context, is not found in the model. It is found in the environment that allows the model to be built — and in the recognition that the researcher behind it is not a depreciating asset, but a compounding one.